Fidelity Perspectives: Strategic insights for 2026

2025 in Review

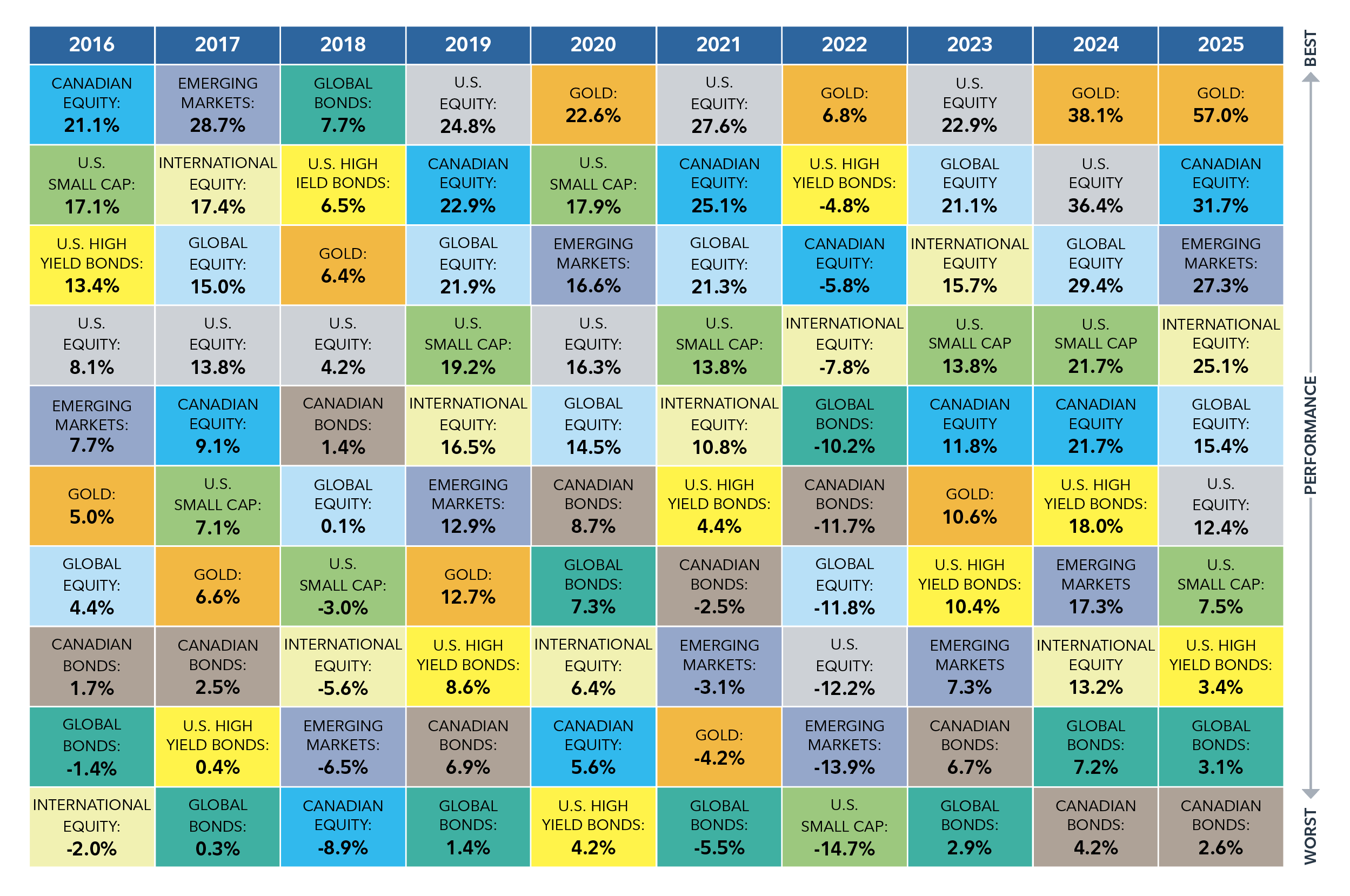

Despite early-year volatility driven by trade tensions and economic uncertainty, global equity markets posted strong gains in 2025. The importance of international diversification came into focus for investors last year as international equities led the way, outperforming their U.S. counterparts amidst fears of the impact of tariffs and valuation concerns, specifically surrounding artificial intelligence (AI)-related stocks. While volatility marked the first half of 2025, global equity markets rallied as improvements to the impact of trade policy set in. U.S. market performance bounced back, with AI-related stocks continuing to drive returns. Despite broad-based gains globally, geopolitical tensions and uncertainty drove investors towards safe-haven investments, sending the price of gold to record highs. Government bond yields stabilized through the year, as major central banks shifted from tightening of monetary policy to gradual rate cuts. Many central banks globally lowered target interest rates this year, motivated by cooler labour dynamics and inflation. The U.S. Federal Reserve (Fed) lowered rates in 2025 by a total of 75 basis points, and the Bank of Canada lowered rates by a total of 100 basis points, citing additional pressures at the beginning of the year due to stress surrounding tariffs.

Chart 1: Calendar year returns of global markets

What’s to come in 2026?

Equity markets proved resilient in 2025, continuing to rise despite volatility and uncertainty. As we move into a new year, equity markets contend with uncertain monetary policy, elevated valuations and simmering geopolitical tensions. AI is expected to remain a central focus, offering significant potential to shape markets and alter how companies operate, innovate, and compete.

Fidelity portfolio managers have weighed in on what investors can expect this year.

| Andrew Marchese |

|---|

Chief Investment Officer and Portfolio Manager Andrew Marchese shares a nuanced perspective on the global investment landscape. His outlook is shaped by four key pillars:

Corporate earnings were surprisingly resilient in 2025, supported by global stimulus and delayed tariff impacts, with forecasts pointing to low double-digit growth in 2026. However, this strength is concentrated in sectors like technology and financials, while autos, housing and transportation have faced prolonged weakness. Historically, these lagging sectors tend to lead early in a recovery cycle, making them areas to watch as monetary and fiscal tailwinds gain traction. Interest rates currently sit near neutral but political pressure in the U.S. for aggressive easing could accelerate rate cuts. Such moves would likely boost economic growth and risk assets but could also distort valuations and increase market volatility. For investors, this means staying alert to policy shifts and their impact on asset pricing. Global liquidity continues to rise, creating a backdrop of asset inflation and pushing investors further out on the risk curve. This abundance of money, combined with resource scarcity and geopolitical shifts, creates a compelling case for hard assets like gold and commodities. Canada’s resource-rich economy stands out as a beneficiary of these trends, offering an attractive long-term investment proposition. Valuations in the U.S. are high but not at the extremes seen during the dot-com bubble. Today’s technology leaders are self-funding their growth, unlike the debt-driven expansion of the late 1990s. Andrew stresses that valuation alone is not a catalyst: durability of earnings matters most. Outside the U.S., many sectors still trade at appealing discounts, offering diversification opportunities for global investors. The key question remains whether earnings and cash flows can sustain current multiples over the long term. In Andrew’s view, AI could eventually serve as a productivity game-changer, helping offset inflationary pressures from excess liquidity. However, he cautions that widespread impact is not imminent. In the meantime, investors must navigate a paradoxical landscape of abundant liquidity, rising resource scarcity, and valuation distortions. Success will require looking beyond the headlines, balancing innovation themes with opportunities in early-cycle sectors, global markets and hard assets. |

| David Wolf, David Tulk, Ilan Kolet |

|---|

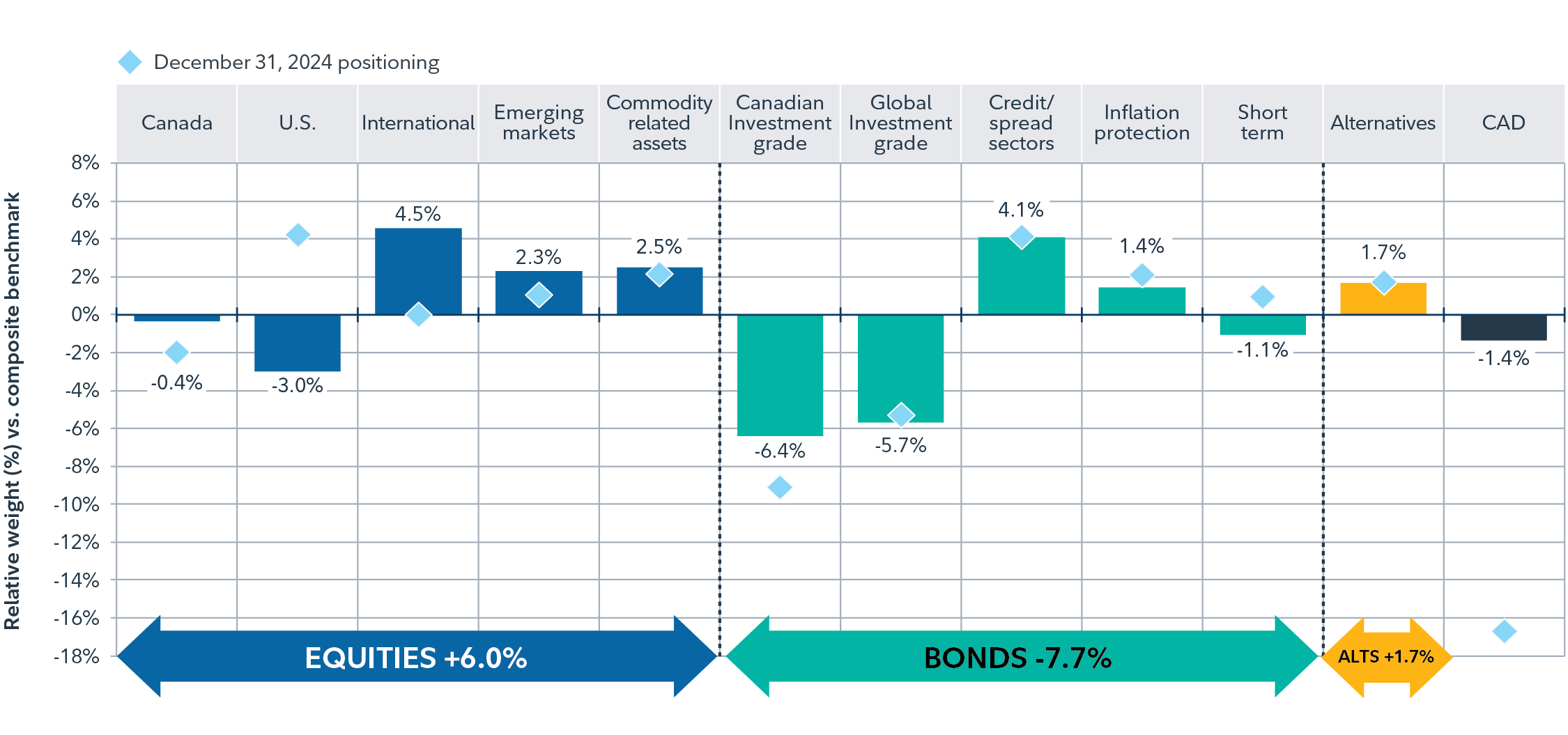

Portfolio Managers David Wolf and David Tulk and Institutional Portfolio Manager Ilan Kolet note that global economic activity remains broadly supportive, with a low risk of recession across major economies, including the U.S. Consumer resilience and strong corporate fundamentals underpin this view, even as labour markets show signs of cooling. However, persistent concerns around U.S. policy credibility – such as political interference with the Fed and recent disruptions to U.S. government data releases — reinforce the case for diversification beyond U.S. markets. The U.S. administration’s focus on weakening the U.S. dollar, combined with fiscal stimulus measures like the One Big Beautiful Bill and potential Fed rate cuts, adds complexity to the outlook. While these factors may support near-term growth, they also heighten currency risk and erode trust in U.S. institutions. As shown in Chart 2, the managers maintain a modest overweight to equity beta, primarily through allocations to international and emerging markets equities, funded by an underweight in U.S. exposure. U.S. equity markets appear increasingly crowded due to the ongoing AI investment theme, though they acknowledge that AI-related capital expenditures have further runway, supporting selective opportunities in technology and large-cap growth. Canadian equities have improved as trade conditions stabilize and fiscal initiatives target infrastructure and resource development, though productivity challenges remain. Reflecting this, the managers have moved from a long-standing underweight allocation in Canadian equities to a more neutral stance. Within fixed income, the managers remain underweight in Canadian and global investment-grade bonds, favouring credit-spread assets and inflation-linked securities to provide resilience against inflation and capitalize on strong corporate fundamentals. Duration exposure is generally underweight versus benchmarks, with U.S. duration shifted toward global duration given the U.S.’s less creditor-friendly environment. On currencies, they maintain reduced exposure to the Canadian dollar in favour of a diversified basket of global currencies, aligning with their broader diversification strategy. Gold positions remain consistent, supported by unresolved U.S. inflation risks and recent signs of re-acceleration, while Canadian inflation appears contained. Bitcoin is not viewed as a tactical opportunity despite recent volatility, as its role relative to existing tools remains unclear. Commodity-related assets continue to play a role in the portfolio as part of a balanced approach to growth and inflation protection. Investor sentiment is constructive but cautious, reflecting optimism tempered by policy uncertainty and inflation risks. The managers advocate for well-diversified portfolios across asset classes, styles and regions to ensure resilience against varied shocks. The Fund’s positioning reflects this philosophy, balancing growth opportunities in international and emerging markets with defensive allocations designed to protect and grow capital over the long term. |

Chart 2: Global Balanced Fidelity Managed Portfolio (FMP) positioning

| Adam Kramer |

|---|

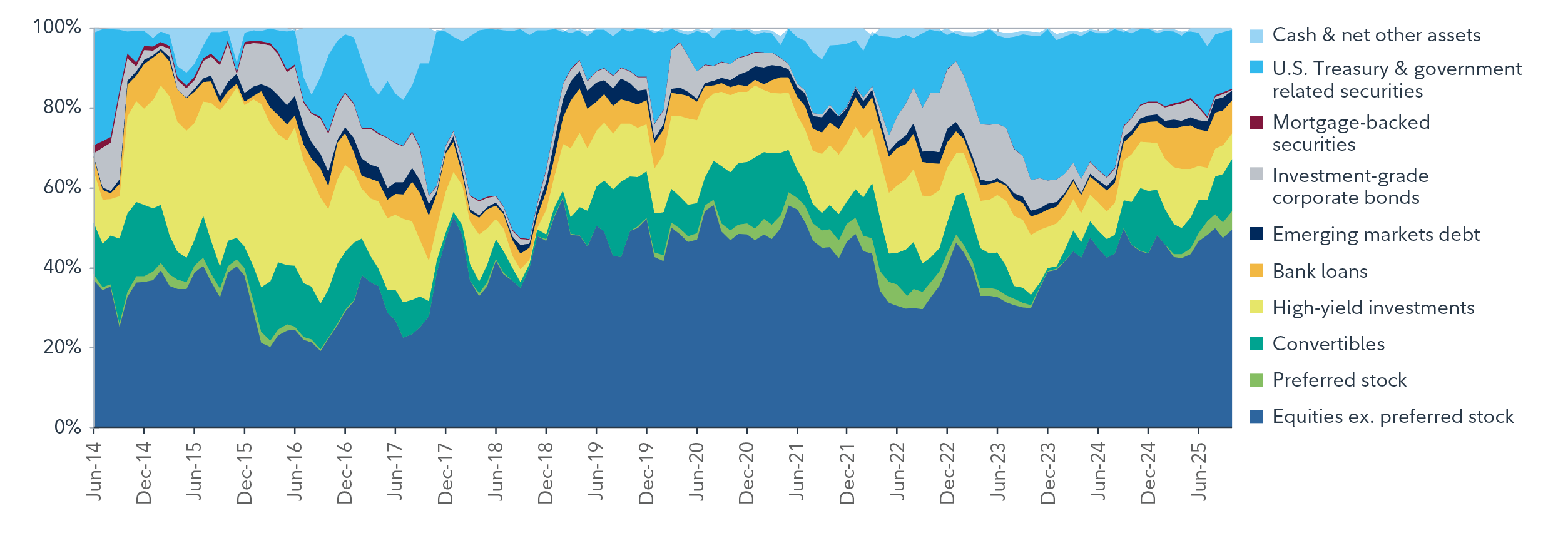

Looking ahead, Portfolio Manager Adam Kramer remains focused on positioning the portfolio with discipline rather than predicting the path of monetary policy or the trajectory of the business cycle in 2026. Adam emphasizes a balanced approach, allocating capital where he sees attractive opportunities while maintaining flexibility to adapt as market conditions change. On the fixed income side, Adam favours long-term U.S. Treasuries, which provide an efficient way to build out Fidelity Tactical High Income Fund’s duration profile while also serving as a defensive hedge against potential market stress. He also sees value in Brazilian local-currency bonds, supported by attractive real yields, the central bank’s restored credibility, and potential political tailwinds ahead given the 2026 election. While exposure to high-yield bonds and leveraged loans has been selectively reduced, Adam remains focused on issuers with strong fundamentals and attractive yields. As demonstrated during the Liberation Day dislocation earlier in 2025, he is prepared to act upon high-conviction opportunities should a spread-widening event create compelling entry points in 2026. Convertibles remain a key differentiator in the portfolio, as they are the only fixed income segment currently trading at mid-cycle valuations, according to Adam. Adam has been identifying attractive opportunities across diverse sectors, including biotechnology, specialty pharmaceuticals, consumer discretionary, battery storage, industrial semiconductors, and software. Looking ahead, Adam anticipates an active new-issue market in 2026, which may provide a strong pipeline of opportunities to generate value. On the equity side, Adam anticipates certain Canadian utility companies may benefit from data-centre expansion, driving power demand and supporting earnings growth, further reinforced by provincial government initiatives to promote technology and infrastructure development over the next five years. Similarly, oil-tanker companies remain attractive as global trade dynamics and OPEC production support strong rates, with balance-sheet improvements and dividend strength adding to the appeal. Additionally, Adam sees strong potential in U.S. small- and mid-cap stocks heading into 2026, with negative sentiment priced in across various industries in his view. He has also added high-quality large-cap dividend payers in pharmaceuticals and major U.S. banks as valuations turned attractive, while reintroducing REITs, pipelines and select energy names. Finally, Adam views the U.S. preferred market as challenged by low liquidity and weaker fundamentals but continues to find select opportunities. These positions could serve as attractive income-drivers in 2026, with the added potential for meaningful principal appreciation if interest rates decline. Every year, markets often, rightly or wrongly, price in negative scenarios. Adam’s approach focuses on uncovering these areas where worst-case outcomes are already reflected in valuations, creating opportunities that may help dampen volatility while offering meaningful upside potential. As we move into 2026, Adam will continue to seek out these dislocations. Chart 3 highlights his track record of rapidly repositioning the portfolio when such opportunities arise: a disciplined approach he intends to carry forward as new catalysts emerge in the year ahead. |

Chart 3: Fidelity Tactical High-Income Fund Historical positioning

Viewpoints from our equity portfolio managers

Global equities

| Mark Schmehl |

|---|

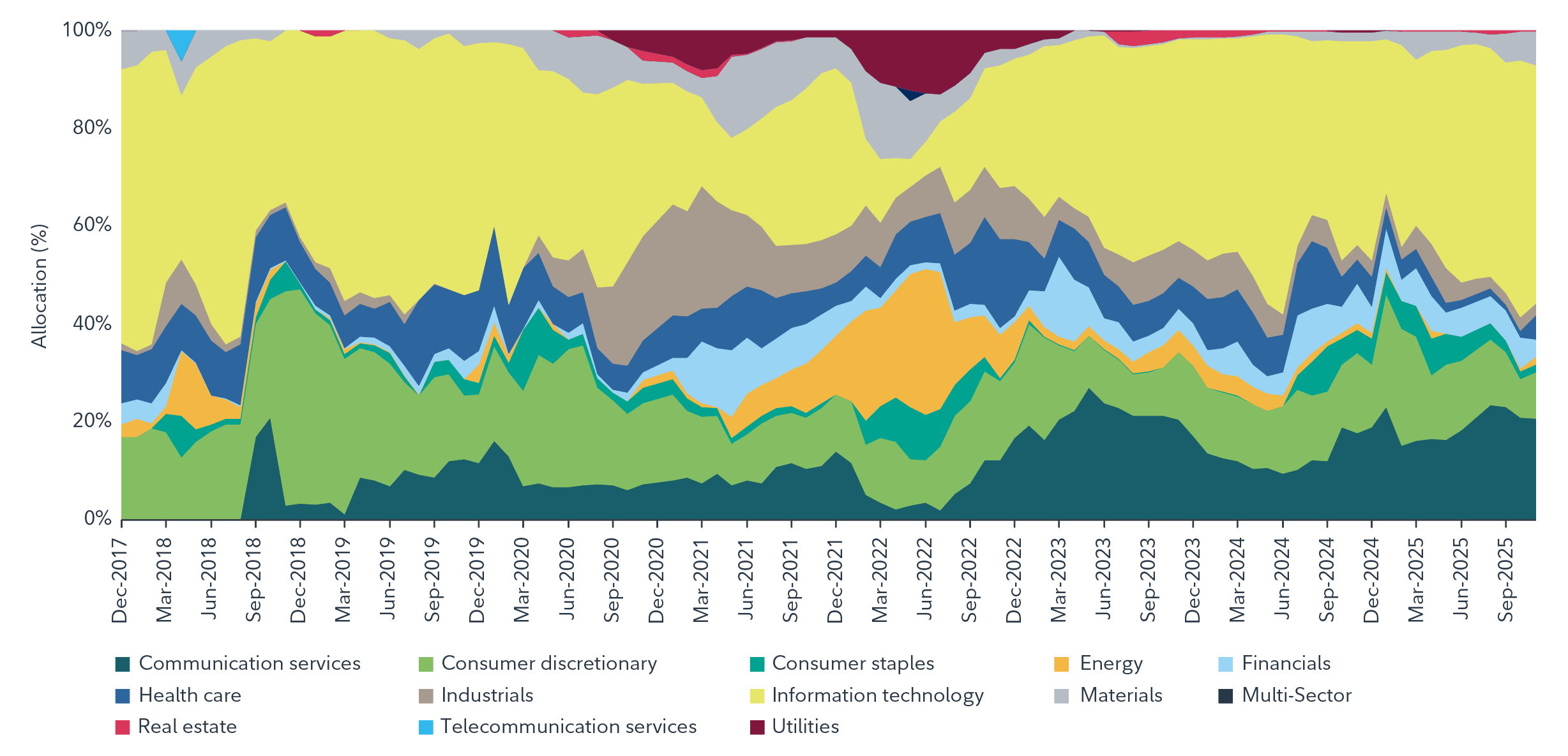

Portfolio Manager of Fidelity Global Innovators® Class, Fidelity Canadian Growth Company Fund, Fidelity Special Situations Fund and Fidelity Global Equity+ Fund, Mark Schmehl anticipates that 2026 will mark a shift in the AI-investment cycle, moving from infrastructure build-out to widespread application. He believes the coming year will be defined by the “magic of using AI,” as businesses and individuals begin to adopt practical tools that transform workflows and streamline inefficiencies. Despite recent volatility and fear-driven selling, Mark remains constructive on the AI-investment theme. He views the Q4 volatility as sentiment-driven rather than a structural shift, noting that demand for computing power remains robust and supply constraints persist. Unlike the dot-com bubble, where infrastructure sat idle, today’s AI hardware is sold out for years to come. In his view, this signals that the cycle is far from over. However, he cautions that adoption may take time, and the market’s impatience could create near-term volatility. Portfolio-wise, his approach remains focused, with concentrated positions in high-conviction ideas. He continues to see compelling opportunities in semiconductor companies powering AI infrastructure, notably Taiwan Semiconductor Manufacturing Company (TSMC), a top-10 holding in Fidelity Global Innovators® Class as at September 30, 2025. TSMC manufactures advanced semiconductor chips that power virtually all modern electronic devices, including smartphones and AI systems. In Mark’s opinion, the company holds a nearmonopoly in leading-edge chip-fabrication, making it one of the most critical players in the global technology supply chain. Despite its critical role, he believes TSMC trades at a meaningful discount relative to peers, presenting attractive upside potential. He also continues to maintain ownership of software firms using AI to drive operational efficiency, including Roblox (another top-10 position in Fidelity Global Innovators® Class as at September 30, 2025). According to Mark, Roblox is transforming the videogaming space by leveraging AI to improve user experience and game development. Mark also maintains exposure to gold as it serves as a diversification tool for his portfolios and is supported by a backdrop of geopolitical uncertainty and inflationary pressures. In addition, he is excited about his exposure to private placements, which he believes is well-positioned to benefit from AI-led growth, and remains active in exploring new private opportunities. Being based in San Francisco provides him with a significant advantage, giving him direct access to the management teams of many transformative companies. This direct engagement allows him to identify emerging trends early and act quickly on new opportunities. Looking ahead for 2026, Mark reaffirms the core focus of his investment strategy: identifying areas of positive change. His flexible approach, as shown in Chart 4, has historically allowed him to capitalize on opportunities as they arise. |

Chart 4: Fidelity Global Innovators® Class historical sector allocation

| Patrice Quirion |

|---|

International equities are increasingly coming back in favour, creating what Patrice Quirion, Portfolio Manager of Fidelity Global Concentrated Equity and International Concentrated Equity Funds sees as attractive opportunities. As a contrarian investor, Patrice believes markets often overreact, and the long period of underperformance following the European financial crisis has led to meaningful valuation gaps that patient, fundamentals focused investors can now exploit. Positive catalysts are emerging. In 2025, Europe has begun to stabilize – supported by progress toward resolving the Ukraine conflict and renewed fiscal stimulus – while Asia is seeing early signs of recovery in China’s real-estate market and improving consumer confidence. With U.S. market leadership increasingly concentrated in a small group of AI driven companies, global diversification is becoming more compelling. Against this improving backdrop, Patrice is identifying opportunities across international markets. He sees particular value in the Chinese consumer sector, where companies remain mispriced relative to global peers, and in the rise of Chinese multinationals that are increasingly competitive on both quality and cost. In Europe, he is finding potential beneficiaries of renewed economic momentum, including firms in construction, homebuilding and infrastructure. Overall, Patrice remains optimistic that improving fundamentals, attractive valuations and broadening global catalysts position international markets well for long term investors. |

| Salim Hart |

|---|

Long overshadowed within equity markets, global micro-caps re-emerged in 2025 as a compelling source of differentiated returns. Early strength in international markets set the tone, followed by a meaningful recovery in North America. Macroeconomic resilience, less disruptive tariff outcomes, and expectations for declining interest rates helped fuel renewed investor confidence, particularly in speculative areas of the market. However, Salim Hart, Portfolio Manager of Fidelity Global Micro-Cap Fund emphasizes that the coming year warrants a more nuanced lens. While lower rates have historically supported risk assets, their ability to spark broad rallies is constrained by high valuations and uneven earnings trends. Rather than chasing crowded trades where consensus assumes every outcome is positive, he remains cautious heading into the new year, adopting a contrarian approach and repositioning his portfolio for quality and resilience. Against this backdrop, Salim is finding compelling opportunities in Europe and Japan, where smaller-cap companies combine local strength with niche, specialty business models, making them less vulnerable to macroeconomic turbulence. Global micro-caps remain a distinct source of alpha, combining differentiated return potential with diversification benefits and downside resilience – key attributes for strengthening portfolios in uncertain markets. Viewing volatility as a strategic advantage, Salim leverages market dislocations to uncover mispricing. In a segment characterized by structural inefficiencies, success hinges on Fidelity’s rigorous research team and selective positioning to uncover hidden pockets of value. |

U.S. equities

| Will Danoff, Nidhi Gupta and Matthew Drukker |

|---|

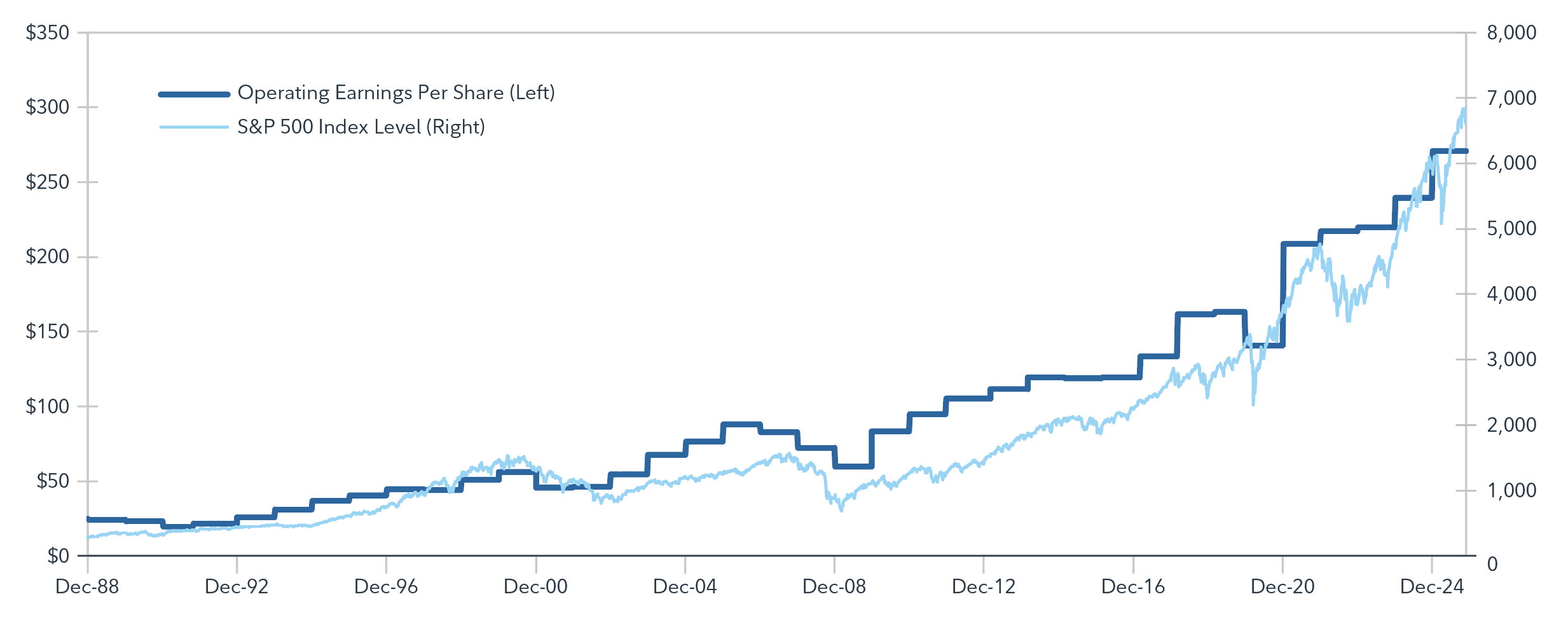

Portfolio Managers of Fidelity Insights Class® Will Danoff, Nidhi Gupta and Matthew Drukker remain focused on companies benefiting from powerful secular trends, particularly advancements in AI, cloud computing, data-centre expansion and industrial modernization. What continues to differentiate this cycle is not only the speed of technological adoption, but the ability of leading companies to translate these developments into sustainable earnings growth, expanding total addressable markets and improved productivity across the economy. These themes remain core to the team’s highest-conviction holdings and are expected to play a central role in driving U.S. equity performance over the coming years. As inflation eases and policy clarity improves, opportunities across small- and mid-cap names that meet the Fund’s criteria for earnings durability and disciplined execution are expanding. Supported by corporate reinvestment and clearer capital spending trends, this backdrop may set the stage for new market leaders to emerge into 2026 and beyond. In 2026, the team maintains a constructive outlook. U.S. corporations continue to reinvest heavily in technological transformation, supporting a reinforcing cycle between innovation and economic growth. Meanwhile, strong balance sheets, healthy earnings trends and stabilizing inflation data may provide a solid foundation for continued strength among U.S. equities. In this environment, disciplined, research-driven stock selection becomes increasingly important, as the portfolio managers place greater value on companies capable of sustaining earnings momentum regardless of macro uncertainty. As seen in Chart 5, historically, stock prices have followed earnings. |

Chart 5: Stock prices follow earnings

| Steve DuFour |

|---|

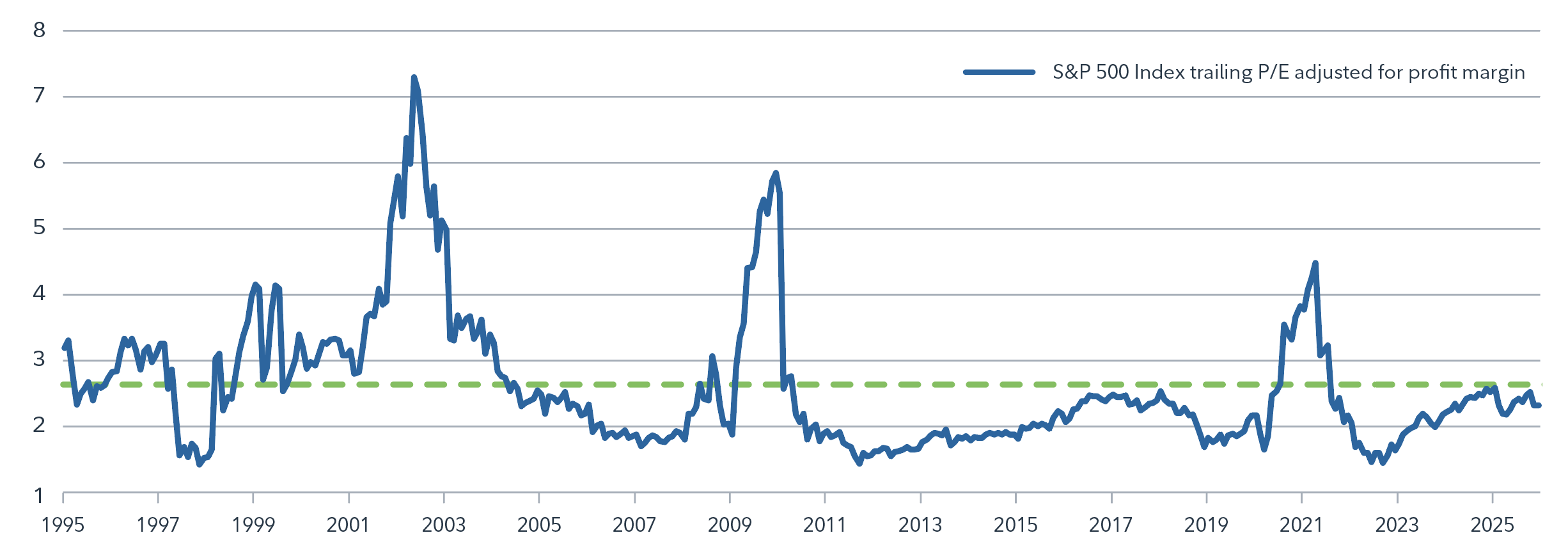

Entering 2026, Portfolio Manager Steve DuFour anchored Fidelity U.S. Focused Stock Fund in long-term secular growth themes, with an emphasis on innovation, technological advancement and the evolving energy landscape. The strategy continues to focus on companies positioned to benefit from these transformative trends, aiming to capture opportunities where technology drives efficiency, enhances customer engagement and supports sustainable earnings growth. Rising power demand and accelerating investment in grid modernization and energy infrastructure continues to broaden the opportunity set beyond traditional technology leaders. Steve emphasizes that the growing imbalance between energy supply and demand must remain a key focus, as accelerating AI innovation and technological advancements are driving energy needs far faster than current infrastructure can support. As in Chart 6, elevated valuations in U.S. equities are being supported by record-high profit margins. This reflects that leading innovative companies are being rewarded with higher prices and stronger multiples driven by profitability, adding stability to the current market advance. Unlike previous periods of rich valuations, such as in 2000 and even 2021, today’s market strength is underpinned by robust earnings and accelerating profitability. Looking ahead to 2026, Steve remains constructive. Corporate profitability is firm, innovation investment is accelerating, and a more stable monetary backdrop should enable companies to refocus on growth, efficiency gains, and technology adoption. In an environment where the market is increasingly rewarding true earnings durability, the Fund aims to stay selective and opportunistic, concentrating capital in high-quality companies with underappreciated relative earnings growth and using short-term volatility to add to long-term winners. Leveraging Fidelity’s robust research platform, Steve continues to position the Fund in businesses he believes are poised to become future market leaders, aiming to drive the Fund’s potential for outperformance across market cycles. |

Chart 6: High profit margins help keep valuations in check.

Earnings multiples look more reasonable relative to record profit margins

| Darren Lekkerkerker |

|---|

Looking ahead to 2026, Portfolio Manager of Fidelity American Equity Fund and Fidelity North American Equity Class Darren Lekkerkerker remains optimistic on the macroeconomic landscape. He highlights the stability of the U.S. economy and cites the strong profitability companies have achieved in 2025, positioning them well for the year ahead. While 2025 presented a volatile and uncertain year for global equity markets, Darren believes North America offers strong investment opportunities, thanks to its robust innovation pipeline, favourable demographics and resource self-sufficiency. Although positive on the current macroeconomic backdrop, Darren continues to emphasize a bottom-up approach, focusing on selecting high-quality companies with strong fundamentals for his portfolios. With a focus on companies with strong fundamentals and long-term growth potential, Darren has found compelling investment opportunities across the consumer discretionary and industrials sectors. Within consumer discretionary, companies with strong brand momentum and growth through expansion have been strong themes across Darren’s portfolios through the new year. Darren has also been finding attractive investment opportunities in the industrials sector, particularly aerospace, as a result of cyclical and secular tailwinds. Driven by cyclical recovery and secular trends such as global economic growth and urbanization, the industry should see supportive growth and sustained demand for air travel and related services. |

Canadian equities

| Dan Dupont |

|---|

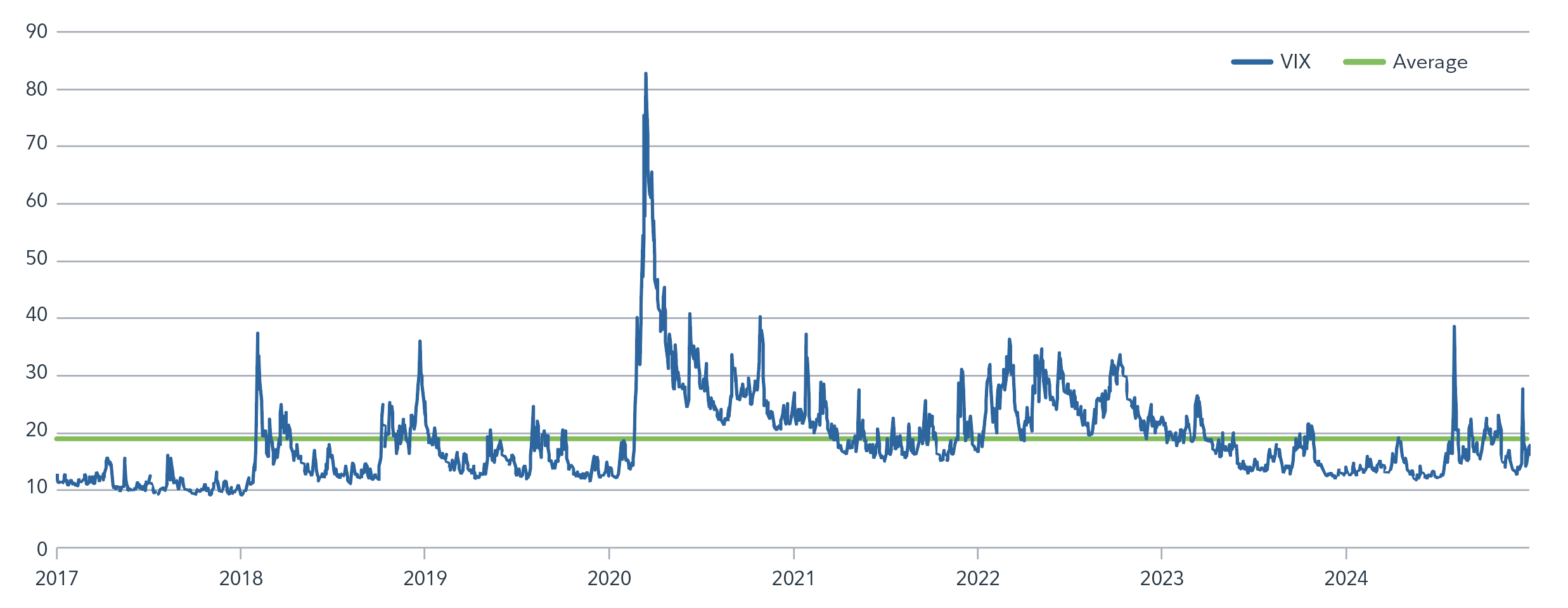

As markets move into 2026, Portfolio Manager of Fidelity Canadian Large Cap Fund, Fidelity Global Value Long/ Short Fund and Fidelity Global Equity+ Fund, Dan Dupont believes investor confidence remains elevated, even as the balance of risks has become more asymmetric. After a brief period of volatility earlier in 2025, markets quickly regained momentum, reinforcing the view that conditions will remain broadly supportive. While this optimism has been rewarded, Dan sees limited margin for error, particularly given elevated valuations and historically strong corporate margins across many regions. Looking ahead, Dan expects 2026 to be shaped less by accelerating growth and more by how markets respond to normalization. Margins remain near cycle highs, especially in the U.S., and even modest pressure on earnings or financing conditions could have an outsized impact on returns. As a result, he believes dispersion across companies and sectors is likely to increase, with greater differentiation between businesses with durable fundamentals and those more exposed to valuation and balance sheet risk. In this environment, his portfolios are positioned with a clear emphasis on defensiveness and flexibility. Rather than forecasting a specific economic outcome, Dan is focused on preparing for a wider range of scenarios. Defensive sectors continue to play an important role, offering stability if growth moderates and serving as a source of liquidity should volatility create more attractive entry points elsewhere. In Dan’s view, volatility may play a more significant role in 2026. After a prolonged period of generous risk pricing, markets may become more sensitive to incremental changes in earnings, credit conditions or policy expectations. Dan views this as an opportunity rather than a threat, as periods of market stress have historically provided compelling moments to reallocate capital into high-quality businesses at improved valuations. |

Chart 7: CBOE VIX Index

Credit conditions remain an important part of the forward outlook. With no traditional credit cycle having played out in many years, Dan believes investors may be underestimating the potential for stress to emerge over time, particularly in areas where leverage has increased, and underwriting standards have weakened. This reinforces a cautious approach to balance sheets and a preference for businesses with financial resilience. Geographically, Dan expects leadership to gradually broaden. While U.S. equities remain supported by strong narratives, valuations reflect high expectations. In contrast, international markets, particularly Europe, offer a more balanced starting point, where returns may be driven more by valuation discipline and normalization than by continued multiple expansion. Within Canada, the outlook remains measured, shaped by elevated household leverage and housing-related risks. As a result, Dan expects returns to be driven primarily by company-specific fundamentals rather than broad macro tailwinds. |

| Hugo Lavallée |

|---|

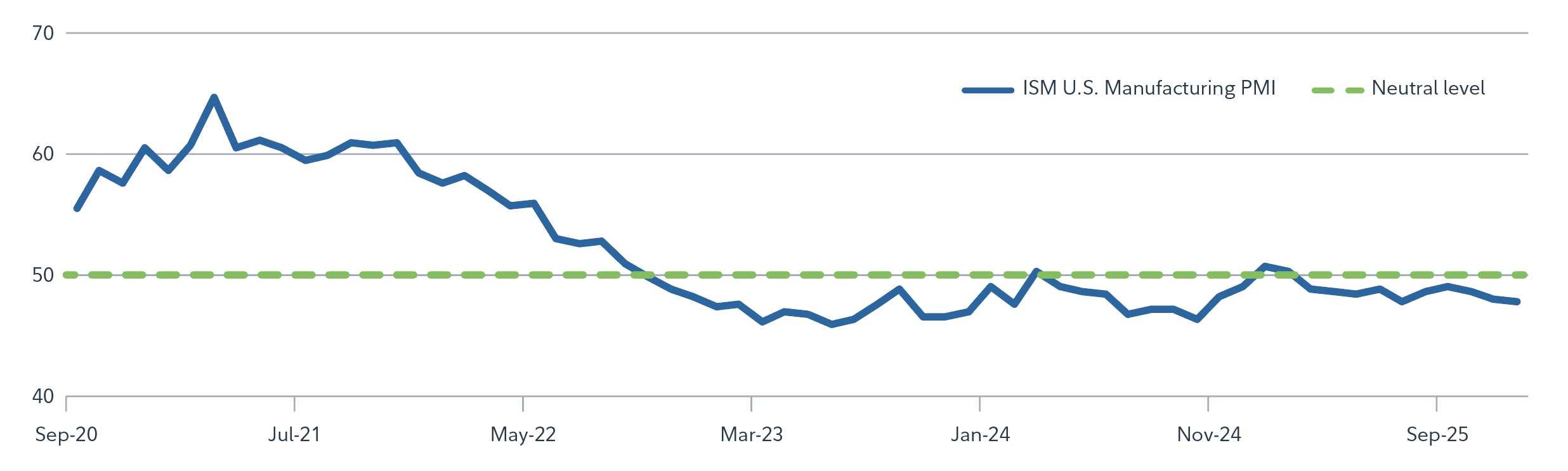

Portfolio Manager of Fidelity Greater Canada Fund, Fidelity Canadian Opportunities Fund and Fidelity Global Equity+ Fund, Hugo Lavallée’s contrarian approach turns volatility into opportunity, investing ahead of the recovery through preparation, patience and a commitment to quality. After a decade-long bear market, Hugo anticipates commodities entering a new phase driven by structural forces: reversing globalization, chronic underinvestment and prolonged interest-rate repression. These dynamics weaken supply-chain resilience and increase systemic vulnerability, while governments aim to lower borrowing costs. Against this backdrop, Hugo anticipates monetary easing and yield curve control to dominate 2026 headlines, reinforcing gold’s role as a hedge. Gold’s strength also creates broader opportunities in Canada, where equities are showing signs of recovery after years of lagging U.S. markets. Supported by a resource-rich economy and favourable cyclical dynamics, Hugo is looking beyond expensive market leaders to “old economy” sectors with compressed margins poised for rebound. Record gold prices highlight its safe-haven appeal, and Hugo is pursuing derivative plays tied to mine expansions and drilling. Transportation follows as a key theme, with a prolonged downturn particularly in logistics and railways, creating attractive entry points. With U.S. Manufacturing PMI signaling contraction for an unprecedented three years, as seen in Chart 8, valuations are deeply discounted, and companies are underearning – conditions he sees as ideal for his contrarian positioning. Regulatory changes tightening driver supply in North America add structural tailwinds for pricing power once demand rebounds. |

Chart 8: U.S. manufacturing PMI fell over the last three years

Elsewhere, Canadian banks, which were relatively subdued in 2024, are now showing improving conditions. Lower rates, potential fiscal stimulus and stronger commodity and emerging-market dynamics favour banks with global exposure. Despite modest domestic growth, the financials sector continues to deliver solid performance, supported by strong fundamentals and attractive valuations. |

Viewpoints from our fixed income managers

| Michael Plage, Celso Muñoz, Stacie Ware and Brian Day |

|---|

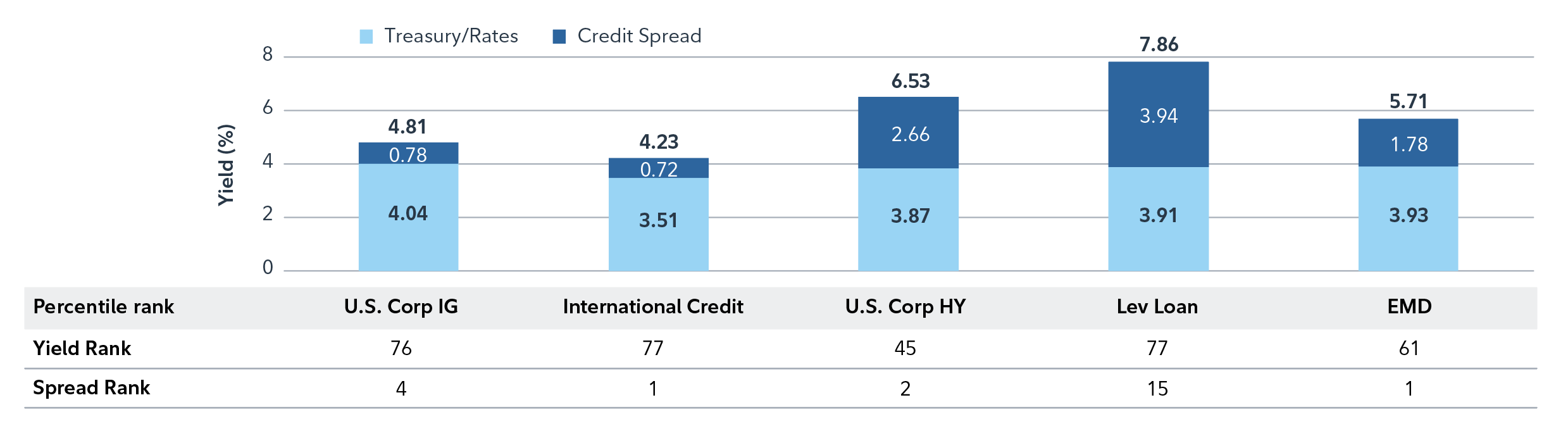

Portfolio managers of Fidelity’s multi-sector fixed income strategies Michael Plage, Celso Muñoz, Stacie Ware, and Brian Day note that 2025 was marked by a dynamic and often turbulent economic backdrop. Evolving trade policies, fiscal initiatives such as the “One Big Beautiful Bill,” and signs of slowing labour markets have created cross-currents for policymakers and investors alike, further clouding the market outlook. Despite these challenges, fixed income markets have continued to post robust returns in 2025, marking three consecutive years of strong performance. Since the “great rate reset” of 2022, 10-year Treasury yields have traded within a 150 basis point range but are currently close to the same levels as three years ago. In contrast, credit spreads have compressed significantly, offering only 40–60% of the compensation historically available across investment grade corporates, high yield, securitized assets, and emerging market debt. As shown in Chart 9, as of December 31, the yield for corporate bonds is 4.81%, which reflects a risk-free rate of 4.04% and a credit spread of 0.78%. Since 2009, the average credit spread has been approximately 1.4%, suggesting that today’s levels are much lower than historical averages - and have been wider 99% of the time - making them vulnerable should a reversion to the mean occur. Against this backdrop, the managers view risk assets as priced for perfection in an imperfect world, leaving little margin of safety should conditions deteriorate. As such, the managers continue to view the risk-reward profile of Treasuries as favourable relative to corporate investment grade sectors and have positioned the multi-sector fixed income strategies accordingly. Looking forward, the managers do not expect the benign credit market to persist indefinitely, but the nature and timing of the catalysts that start the reaction, or the severity of the downturn, remains uncertain. For example, recent bankruptcies, such as those of First Brands and Tricolor, may be emblematic of potential vulnerabilities in credit markets, while the extremely heavy supply of AI/data-centre related bonds poses a risk to the technical backdrop. In light of the frothy valuations in credit sectors, the managers are remaining patient, preferring the liquidity and security of U.S. Treasuries until the market more appropriately reflects the risks inherent in the current climate, at which point U.S. Treasuries will become the source of funds for opportunities in credit markets. Furthermore, given tight spreads, the managers remain confident that a flexible multi-sector approach to fixed income will provide investors with valuable yield, diversification and liquidity benefits in a balanced portfolio. |

Chart 9: Yield

Bitcoin

| Reetu Kumra |

|---|

Portfolio Manager of Fidelity Advantage Bitcoin ETF® and Fidelity Advantage Ether ETF®, Reetu Kumra remains constructive on the outlook for digital assets, supported by both secular and cyclical factors. On the secular side, continued innovation in blockchain technology and decentralized finance is expected to broaden real-world applications, reinforcing crypto’s role in global financial infrastructure. Regulatory clarity is also improving, with initiatives such as the Digital Asset Market Clarity Act and stablecoin legislation creating guardrails that encourage institutional participation and reduce systemic risk. While the next bitcoin-halving is not expected until 2028, structural supply constraints combined with growing adoption should support long-term price appreciation. From a cyclical perspective, crypto’s performance will depend on liquidity conditions and monetary policy. If fiscal stimulus and accommodative central bank actions persist, digital assets could benefit, though volatility may remain a defining characteristic of this asset class. Reetu emphasizes that cryptocurrency offers unique diversification benefits and exposure to a high-growth segment of the financial ecosystem. Unlike gold, which is considered risk-off, bitcoin is a risk-on asset, making it attractive for investors seeking asymmetric upside potential. Beyond price speculation, crypto represents a technological shift toward decentralized finance – one that could reshape payment systems, asset custody and cross-border transactions over the next decade. From a portfolio perspective, Reetu advocates a disciplined approach. She believes bitcoin can serve as a strategic diversification tool: a modest allocation – typically 1–3% of a portfolio – could enhance risk-adjusted returns over the long term. Crypto complements modern portfolio theory by adding an uncorrelated asset class, which is particularly valuable in scenarios where traditional assets such as stocks and bonds exhibit high correlation, as seen in 2022. Looking ahead, Reetu observes that digital assets have evolved from a niche concept to a multi-trilliondollar market commanding investor attention. While volatility and leverage risks persist, the long-term case rests on technological innovation, decentralization and institutional adoption. Alternatives, including crypto, provide a pathway to enhance diversification and resilience in an era where traditional models like 60/40 are being redefined. |

Fidelity All-In-One ETF suite

| Étienne Joncas-Bouchard |

|---|

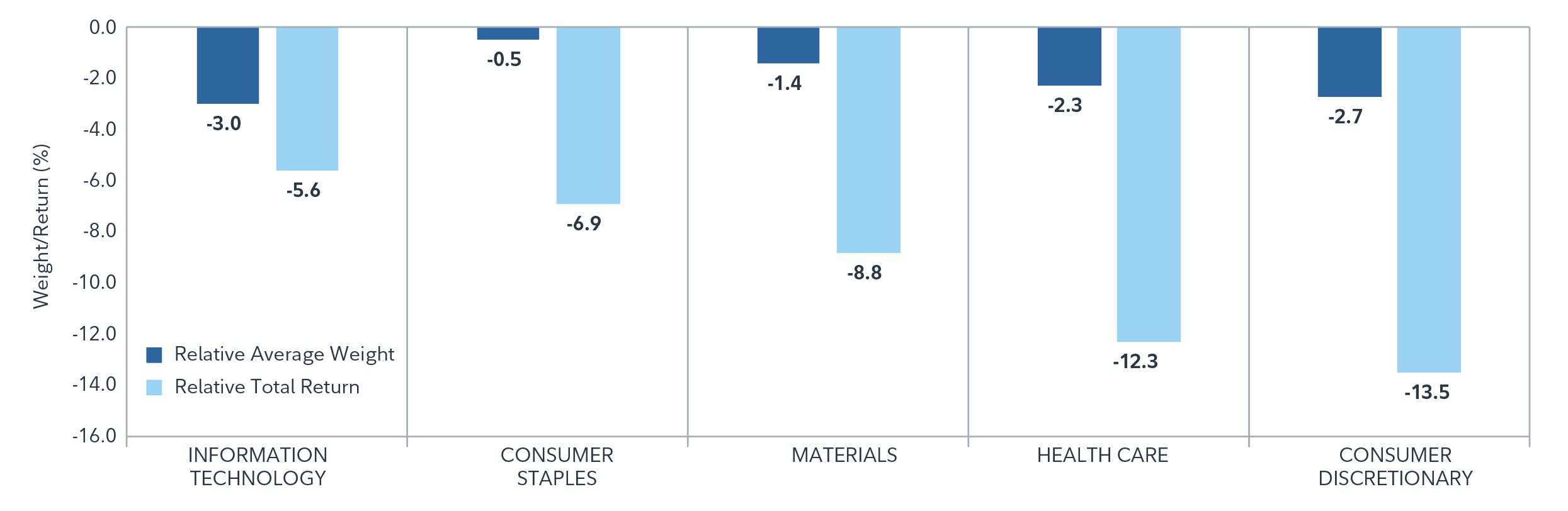

Director of ETF and Alternatives Strategy Étienne Joncas-Bouchard noted that the Fidelity All-In-One ETFs saw record inflows in 2025, highlighting strong investor demand against a rapidly shifting market backdrop. Conditions changed quickly throughout the year: Q1 was marked by trend continuation followed by a brief risk-off period tied to U.S. tariff policy changes – an environment that benefited factors like low volatility and value. Leadership shifted from Q2 onward, as U.S. momentum and growth rally drove anti-factor equities such as low quality, high volatility, and high valuation – typical of early recovery phases. However, as fundamentals regained focus later in the year, the Fidelity All-In-One ETFs delivered stronger results in Q4, reinforcing their long-term resilience. Étienne also observed that the Fidelity All-in-One ETF suite stood out as a key beneficiary of international equity market outperformance in 2025. These globally diversified, multi-asset portfolios include allocations across Canadian, U.S. and international equities, complemented by fixed income and cryptocurrency exposure, depending on the solution. Over the course of 2025, international market exposure was a notable contributor to the Fidelity All-in-One ETF suite’s performance, specifically driven by the strength of the value and momentum factor that also supported the Fidelity All-International Equity ETF (FCIN). This relative outperformance of the international equity sleeve is in large part due to favourable relative sector exposure versus a broad benchmark index like the MSCI EAFE Index. As shown in Chart 10, the international component of the Fidelity All-in-One ETFs (which can be represented by the Fidelity All-International Equity ETF) was underweight the five sectors with the worst relative performance year-to-date. All in all, 2025 underscored the importance of geographic diversification, in Etienne’s view. While international markets led at the start of the year, U.S. equities regained momentum in the mid- to late-stages of the year. Looking ahead, pinpointing which region, style or factor will take the lead can be hard to predict. That’s where a solution like FCIN or a Fidelity All-in-One ETF may add value. FCIN delivers diversified exposure across equity factors, while the Fidelity Allin-One suite offers varied exposure across regions, factors and asset classes. For investors seeking a simplified way to gain diversified exposure, FCIN and the Fidelity All-in-One suite offer a convenient, all-in-one way to stay positioned for opportunity, no matter which market takes the lead in 2026. |

Chart 10: Fidelity All-International Equity ETF relative positioning and sector performance across bottom-performing sectors*

What investors should keep in mind as 2026 unfolds

As we reflect on a year that showcased the strength of global markets and the power of innovation, many investors are turning toward the year ahead with anticipation of what’s next. Will the calm of accommodative central banks and improving trade dynamics bring stability or will hidden risks emerge from beneath the surface?

History reminds us that markets have weathered countless challenges, from economic shocks to policy pivots; however, through every cycle, opportunity has prevailed for those who stayed the course. For instance, if $100,000 CAD was invested in the U.S. stock market 35 years ago, it would be worth approximately $6.1M on December 31, 2025.

The message is clear: stay invested, diversify and rise above the noise. Through active management and thoughtful diversification, portfolios can do more than keep pace – they can thrive.

The future belongs to those who invest for it.

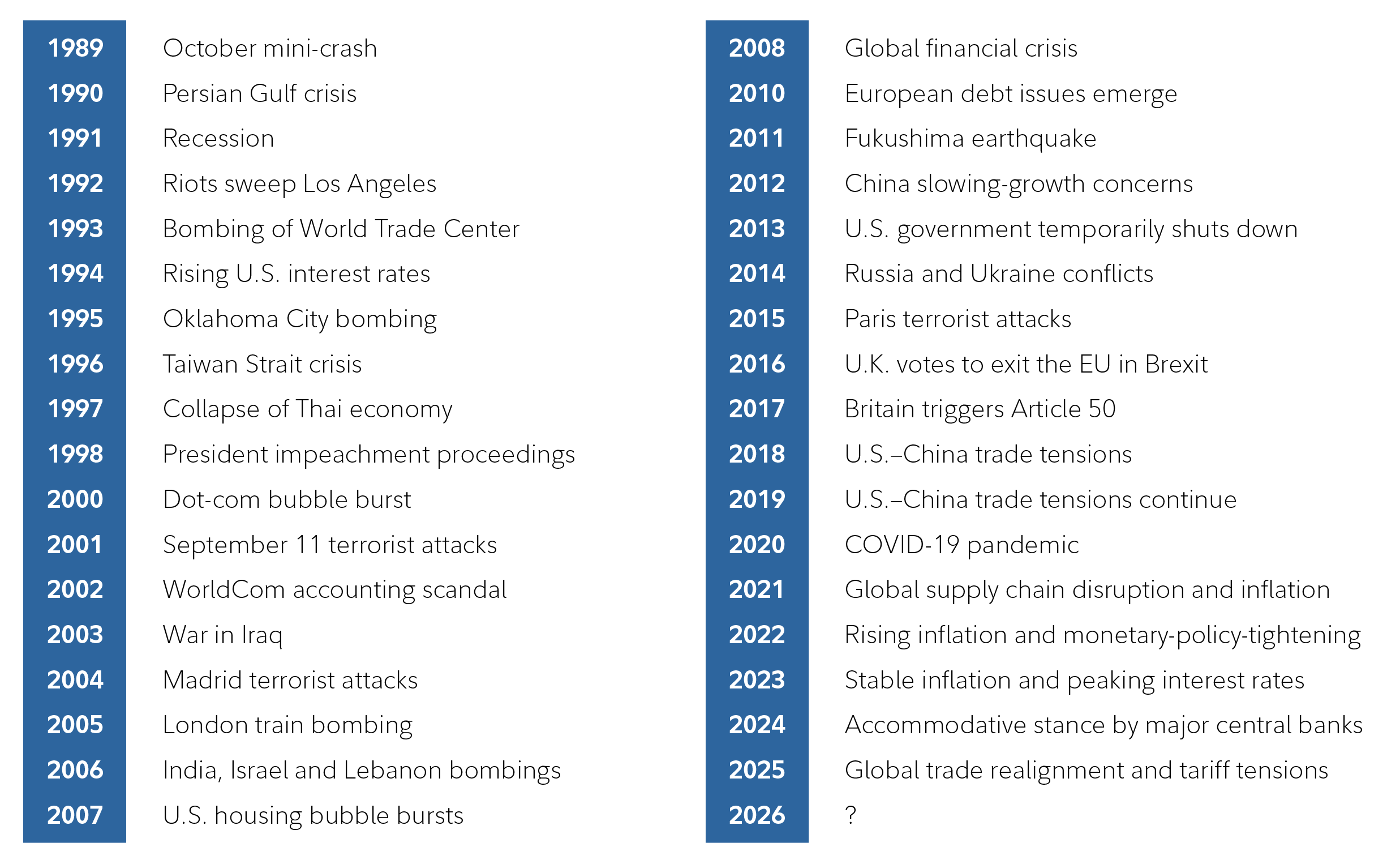

Chart 11: Remember these events?

For more information, please visit fidelity.ca or contact your Fidelity team.