What is a bond?

Bonds have three major components: the face value (also called “par value”), a coupon rate and a stated maturity date.

A bond* is essentially a loan an investor makes to the bond’s issuer. That issuer can be a federal, provincial, state or municipal government or its agencies, a corporation (start-ups to Fortune 500 companies), a private institution (such as a hospital or college) or a foreign government or corporation (of emerging or developed nations).

The investor, or bond buyer, generally receives regular interest payments on the loan (often twice a year) until the bond matures or is “called,” at which point the issuer repays the principal to the investor. Bond funds pool money from many investors to buy individual bonds according to the fund’s investment objective.

Most bonds pay regular interest until the bond matures.

Callable bonds allow the issuer to repay the bond before maturity.

Zero-coupon bonds offer a deep discount and pay all the accumulated interest at maturity.

Who issues bonds?

Governments, government-sponsored enterprises and corporations issue bonds to raise money for their endeavours. The financial health of the issuer determines how highly (or not) the bonds are rated. Higher-rated bonds are considered to be safer, and therefore pay less interest, while lower-rated bonds pay higher interest rates to compensate investors for taking on more perceived risk. An issuer’s credit rating can change in either direction over time.

A summary of the types of bonds and information on their issuers follows.

Federal government bonds

The Canadian government issues bonds to pay for government activities and service the national debt. Canadian government bonds are considered to be extremely low-risk if held to maturity, since they are backed by the Canadian government. Because of their safety, they tend to offer lower yields than other bonds.

Agency bonds

Government-sponsored enterprises issue bonds to support their mandates, which typically involve ensuring certain segments of the population – such as farmers, students and homeowners – are able to borrow at affordable rates. Yields are higher than government bonds, reflecting their higher level of risk, although agency bonds are still considered to be on the lower end of the risk spectrum.

Provincial, state or municipal bonds

Provinces, states and cities issue bonds to pay for public projects (roads, sewers) and finance other activities. Local governments tend to be more risky than the federal governments, and as a result, the yields on local government bonds tend to be relatively higher. However, these bonds tend to offer lower yields than corporate bonds.

Corporate bonds

Corporations issue bonds to expand, modernize, cover expenses and finance other activities. Their yield and risk are generally higher than for government and municipal bonds. Rating agencies assess the credit risk by rating the bonds according to the issuing company’s perceived creditworthiness.

Mortgage-backed securities

Banks and other lending institutions pool mortgages and “securitize” them so investors can buy bonds that are backed by income from people repaying their mortgages. This raises money that allows lenders, in turn, to offer more mortgages. Mortgage-backed bonds have yields that typically exceed those of high-grade corporate bonds. The major risk of these bonds is that borrowers might repay their mortgages in a “refinancing boom,” which could have an impact on the investment’s average life and potentially its yield. These bonds can also prove risky if many people default on their mortgages.

High-yield bonds

Some issuers simply are not as creditworthy as others. These can include local and foreign governments, but generally high-yield bonds are corporate bonds issued by companies that are considered to be at greater risk of not paying interest and/or returning principal at maturity. As a result, the issuer will pay a higher rate to attract investors to take on the added risk. Ratings agencies such as Standard & Poor’s, Moody’s and Fitch evaluate the financial health of a bond issuer and assign a rating that indicates their opinion of whether the bond is investment grade or not. Bonds rated below investment grade are considered speculative and higher-risk.

How a typical bond works

Bonds have three major components.

The first is the face value, also called “par value.” This is the value the bondholder will receive at maturity unless the issuer defaults. Investors pay par when they buy the bond at its original face value. If bonds are retired by the issuer before maturity, bondholders may receive the par value or a slight premium. The price investors pay when buying on the secondary market (in other words, not directly from the bond’s issuer) may be more or less than the face value. See “ Bond prices, rates and yields.”

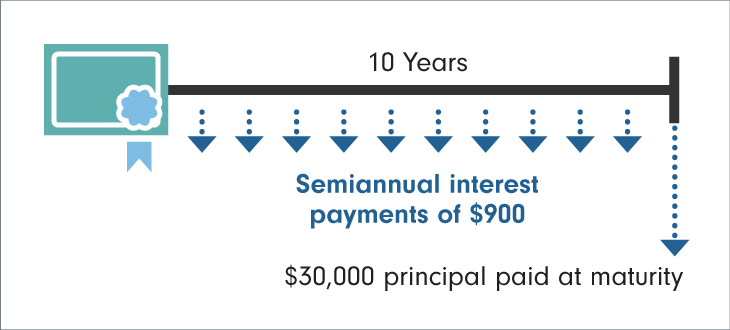

Bonds also have a coupon rate. This is the annual rate of interest payable on the bond. (The term “coupon” dates back to the time when bond certificates were issued on paper and had actual coupons that investors would detach and bring to the bank to collect the interest.) The higher the coupon rate, the higher the interest payments the owner receives. With fixed-rate bonds, the coupon rate is set at the time the bond is issued and does not change. Most bonds make interest payments semiannually, although some bonds offer monthly and quarterly payments.

Third, bonds have a stated maturity date. Generally, this is the date on which the money loaned to the issuer is repaid (assuming the bond doesn’t have any call or redemption features).

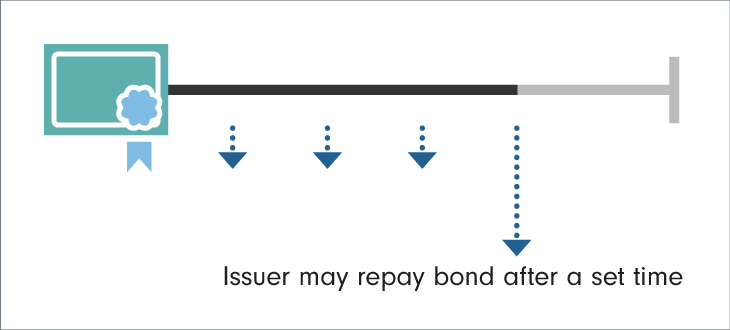

Callable bonds

Callable bonds are bonds that the issuer can repay early, sometimes after a period of several years, at a predetermined price. The attraction of callable bonds is that they typically offer higher rates than non-callable bonds.

However, callable bonds carry call risk. If interest rates drop low enough, the bond’s issuer can save money by repaying its callable bonds and issuing new bonds at lower coupon rates. If this happens, the bondholders’ interest payments stop, and they receive their principal early. If the bondholders then reinvest the principal in bonds with similar characteristics (such as a similar credit rating), they will likely have to accept a lower coupon rate, one that is more consistent with prevailing interest rates. This will lower monthly interest payments.

Example: A callable bond

An investor purchases a $30,000 ten-year callable bond paying 6.5% interest, which is a higher interest rate than similar non-callable bonds. The bond is callable after five years at a price of 103 – that is, 103% of the face value, or $30,900. If interest rates drop enough, the investor may wind up having the principal returned and, when seeking to reinvest the principal, be looking at yields that have fallen since the time of the original investment.

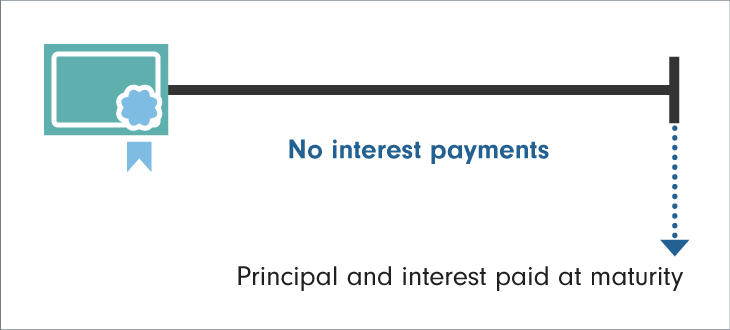

Zero-coupon bonds

Zero-coupon bonds, also known as “strips,” are bonds that do not make periodic interest payments (in other words, there’s no coupon). Instead, the bond is bought at a discounted price, and the investor receives one payment at maturity. The payment is equal to the principal invested plus the accumulated interest earned (compounded annually to maturity).

Zero-coupon bonds are attractive when there is a defined objective and date, such as when a child starts college. The investor receives the principal and interest in one lump sum at maturity.

Example: A zero-coupon bond

Let’s say a couple is saving for their child’s college education, which will begin in ten years. They could buy a ten-year zero-coupon bond that costs $16,000, with a face value of $20,000. In ten years, at maturity, they will receive the face value of $20,000.

Zero-coupon bonds have a few drawbacks. First, in most cases, taxes are payable annually on the interest, even though the interest is not received until maturity. This can be offset by buying the bonds in a tax-deferred retirement account, or in a custodial account for a child in situations where the child pays little or no tax.

Zero-coupon bonds can also be volatile in the open market, and particularly susceptible to interest rate risk. This doesn’t matter if the bonds are held to maturity. But if sold early, a substantial loss can occur.