What is a bond?

| Tip | Bonds are generally considered to be low-risk investments, but high-yield bonds issued by smaller companies and emerging market governments are obviously riskier and, in that sense, more like equities. Individual bonds may be the best known type of fixed income security, but the category also includes fixed income funds, ETFs, GICs, and money market funds. Fixed income funds are professionally managed portfolios that invest in individual fixed income securities. |

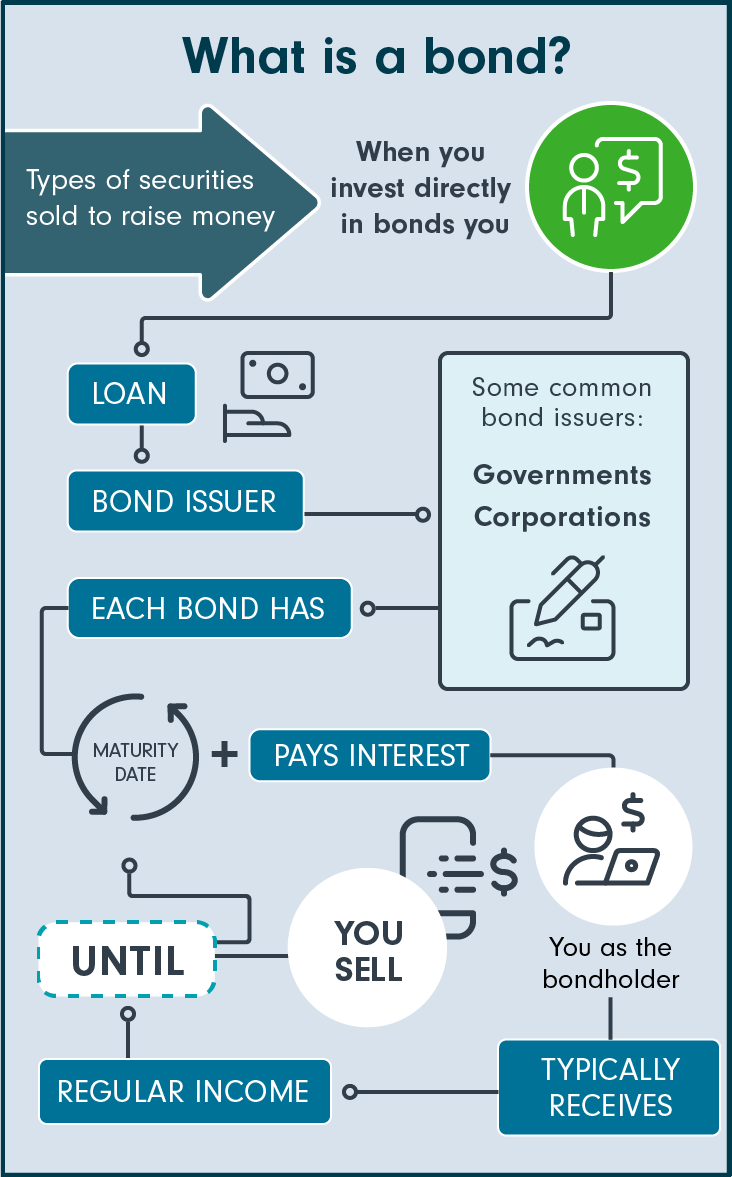

How do bonds work?

Bonds – or fixed income investments – appeal to different investors for different reasons: as an investment style, as a safe investment during times of economic downturn, to offset low-interest-rate environments, to supplement income or as a key part of retirement planning. Investors can buy individual bonds through a broker or directly from an issuing government entity, or buy bond funds.

Bondholder (you) |

Purchase Bondholders provide capital (principal) to the bond issuer, meaning you lend money for a predetermined amount of time (the maturity) to a borrower, who uses your money. |

Bond issuer (borrower) |

Bondholder (you) |

Interest payments The bond issuer promises to pay a set amount of interest on a predetermined schedule, meaning you get regular interest payments on the money you loaned. It also has an interest rate that’s agreed to in advance and referred to as the “coupon,” and that is set out as a percentage of the bond’s face value. So when investors buy a bond, they receive a regular income until it reaches its maturity date. |

Bond issuer (borrower) |

Bondholder (you) |

Principal returned At the end of the term, or when the maturity is reached, the bond issuer typically returns the original capital or principal: the bond issuer repays the bondholder. |

Bond issuer (borrower) |

Say you buy a bond with a face value of $100, a coupon of 8% and a maturity of 10 years. This means you’ll receive a total of $8 of interest per year for the next ten years, plus your original $100 on maturity. The exception is zero-coupon bonds, which only pay out at maturity.

Simple, right? Well, not so fast, because there’s a difference between a bond’s face value and its price. If a bond issuer is seen as risky (i.e., there’s a possibility it won’t be able to repay the face value on the maturity date), a bond with a face value of $100 may only sell for $90. Investors can keep track of a bond’s coupon in relation to its price by looking at what’s called its yield – its coupon divided by its price. In this case, the yield would be 8.9%: 8 (the coupon) divided by 90 (its current price). Companies and countries which are seen as safer will pay lower yields, and those which appear less safe will pay higher yields.